Finance

Nigeria has closed Africa’s biggest Eurobond’s issuance this year, and might raise more

Earlier this week, Nigeria successfully issued three tranches of Eurobonds on the international capital markets, its first such operation since November 2018. While the country had planned to raise between $3bn and $6.2bn, the order book peaked at a whopping $12.2bn, enabling the government to settle for a healthy $4bn from foreign investors. The issuance successfully attracted bids from Europe, the Americas and Asia and was also open to domestic investors. Nigeria now has an extra $4bn split into three tranches: a 7-year tenor Eurobond at 6.125% for $1.25bn, another 12-year tenor Eurobond at 7.375% for $1.5bn and finally a 30-year tenor Eurobond at 8.25% for $1.25bn. While the rates secured by Nigeria are not as attractive as some of its neighbours (Côte d’Ivoire and Benin recently closed Eurobonds issuances at only 4.3% and 4.875%), the operation certainly confirm investors’ appetite for Nigerian debt. Nigeria is rated B2 (negative) by Moody’s, B- (Stable) by S&P and B (Stable) by Fitch. The country is in the middle of a historic foreign exchange and currency crisis, so the influx of additional dollars is expected to help its central bank provide much-needed foreign exchange to the economy. While the proceeds from the Eurobonds are to be used to partly finance the 2021 deficit, an inflow of foreign exchange is also good to increase external reserves and help support the Naira’s exchange rate. The country’s external liquid reserves have been back above the $35bn threshold since mid-September, a level not achieved since last February. While Nigeria has struggled to increase oil production, strong commodity prices still helped the country’s oil exports revenue hit a 3-year high in Q2 2021. Nigeria’s oil & gas exports currently represent 89% of the country’s total export revenues including 80% of crude oil and 8.5% for LNG. The country now has the option of selling more debt: its issuance confirmed the willingness of investors to provide capital and possibly reach the maximum target of $6.2bn Nigeria had set. In an emailed response to Bloomberg this week, Debt Management Office Director General Patience Oniha said Nigeria might seek to raise the full $6.2bn from Eurobonds if the tenors and pricing are good.

Read more »

AFC creates new asset management division – wants to raise $2bn for African infrastructure

The Africa Finance Corporation (AFC) plans to step up its infrastructure financing in Africa with a new asset management division, AFC Capital Partners. Its debut offering, the Infrastructure Climate Resilient Fund (ICRF) is planning to raise $500m within the next twelve months and $2bn over the next three years. The fund will act as a direct investor and a co-investment fund to support key projects across the continent such as ports, roads, bridges, rail, telecommunications, clean energy, and logistics. The AFC has made it clear that sustainable infrastructure will be at the core of its activities by appointing Ayaan Zeinab Adams as the CEO of AFC Capital Partners. She is the former head of the private sector arm of the Green Climate Fund under the UN Framework Convention on Climate Change, as well as a former CIO and Senior Manager of the World Bank Group’s International Finance Corporation (IFC). Ayaan played a key role in building the mandate of the Green Climate Fund Private Sector Facility and rapidly scaled its portfolio within three years to US$2.1 billion invested across Africa, Asia-Pacific, Latin America, and the Caribbean. She also previously also served as UK-based CDC Group’s Managing Director of Africa Funds.

Read more »

Flutterwave and MTN forge new mobile money partnership across Africa

MTN and Flutterwave have announced a mobile money partnership that will allow businesses integrating Flutterwave in Cameroon, Côte d’Ivoire, Rwanda, Uganda and Zambia to receive payments via MTN Mobile Money (MoMo). MTN MoMo is a fintech platform providing consumers and businesses with an electronic wallet, enabling electronic transfers and payments as well as access to digital and financial services. At the end of June 2021, it had 48.9 million active users and 581,514 merchants. MoMo enables businesses to accept and make payments within the mobile money ecosystem. This new partnership will enable Flutterwave to offer MTN Mobile Money as a payment method to its business customers. In recent years, Africa has witnessed an explosion in mobile penetration as smartphone adoption has risen rapidly. According to the GSMA, this year Africa will hit the half a billion mark of unique mobile subscribers and the continent will reach 50% subscriber penetration by 2025. Sub-Saharan Africa alone is responsible for more than 45% of the world’s mobile money accounts with the number of account holders exceeding half a billion by 2020, as shared on Statista. Through this partnership, MTN and Flutterwave will positively contribute to this trend by increasing mobile money usage and penetration in Africa to improve local economies and livelihoods as well as create opportunities for individuals and businesses across the continent. As we progress on our journey to becoming the largest fintech platform in Africa, we will empower millions of businesses to embrace e-commerce in our markets to accept digital payments from MoMo consumers. We believe this is an enabler to accelerating digitized payments in Africa. Serigne Dioum, Chief Digital and Fintech Officer, MTN Group The new partnership will further expand on Flutterwave’s previous collaboration with MTN, beyond Uganda and Rwanda – with the potential of deepening adoption of digital payments and e-commerce in Africa, a sector expected to reach $29 billion by 2022, according to Statista.

Read more »

Sonangol posts $4bn loss for 2020

Angola’s national oil company Sonangol has posted a net loss of Kz 2,383,978,740,444, or the equivalent of $4.1bn for 2020. The crash of oil prices last year along with Sonangol’s impairments were the major reasons behind losses last year. The company continues to be involved in a major restructuring and divestment effort in order to rationalize its operational footprint and prepare for an IPO before 2025. Earlier this year, Sonangol notably launched its Partial Divestment Process (“Processo de Alienação Parcial”) to generate cash for the state coffers by divesting stakes in some of Angola’s key producing offshore blocks along with producing licenses in shallow water and offshore exploration zones. Deals on offer include up to 8.28% in Block 18, up to 10% in Block 15/06 and Block 31, 15 to 20% in Block 3/05 and Block 4/05, 30 to 65% in Block 5/06 and 30 to 70% in Block 23 and Block 27. Supported by the recovery in oil prices, this divestment exercise has generated significant interest amongst E&P players: while proposals were to be submitted by August 6th, Sonangol had to extend the deadline to access the data room until August 20th and extended the submission deadline to September 20th.

Read more »

Nigerian institutional investors back bonds issuance from country’s leading free zone

The Lagos Free Zone Co. (LFZC), a subsidiary Singaporean conglomerate Tolaram, has successfully issued a NGN 10.5bn 20-year Series 1 Senior Guaranteed Fixed Rate Corporate Infrastructure Bonds, the company said today. The issuance falls under a NGN 50bn debt issuance programme aimed at securing financing to expand what has become Nigeria’s most modern and integrated free zone, located on the outskirts of Lagos. The Lagos Free Zone is being developed along with the Lekki Deep Sea Port and will be the largest integrated port-based economic zone in Nigeria. It is being developed over 830 ha as part of a $2.1bn investment commitment by Tolaram, of which about half has been invested already. The company is expected to complete the deep sea port in 2022, at the same time when it would lay out a piped gas supply and distribution network to provide energy to its tenants. The port is currently under construction by the China Harbour Engineering Co. (CHEC) and will have its container terminal operated by CMA Terminals. Its Phase 1 development involves 2 container berths and one dry bulk terminal, with a capacity of 1.2 million TEUs and a draught of 16.5m. The bonds issuance announced this week is significant for Nigeria where unlocking domestic institutional capital remains a priority to bridge the infrastructure financing gap. The bond was backed by an irrevocable and unconditional guarantee from InfraCredit and was accorded a ‘AAA’ long term credit rating by Agusto and Co. and GCR, reflecting the highest degree of creditworthiness for these bonds. It was also oversubscribed by institutional investors including eleven domestic pensions funds, two insurance firms, banks and HNIs. “The transaction is the first 20-year non-FGN Bond issue in the Nigerian debt capital market and the first Securities and Exchange Commission approved Infrastructure Bond for the development of an industrial hub” LFZC said in a statement. Source: PenCom The latest data available from Nigeria’s National Pension Commission shows that the country’s pension funds have continued to shy away from investing in infrastructure funds. Despite a YoY growth of pension funds’ investments into infrastructure funds of +23% between July 2020 and July 2021, they still represent only 0.52% of Nigerian pension funds’ overall investment portfolio.

Read more »

Lagos State prepares for historic green bond issuance

The Lagos State Government is preparing for the issuance of an NGN 25bn ($60m) green bond under the Nigerian Green Bond Market Development Programme (NGBMDP). State Governor Babajide Sanwo-Olu signed an MoU towards the issuance with the NGBMDP’s implementing partners, FMDQ Holdings and Financial Sector Deepening (FSD) Africa this week. The NGBMDP was launched in 2018 by FMDQ, FSD Africa and the Climate Bonds Initiative to support the growth of Nigeria’s non-sovereign debt capital market. It notably supported the development and issuance of Nigeria’s Green Bond Issuance Rules by the country’s Securities and Exchange Commission (SEC) in November 2018 and provided technical support to several issuers. Nigeria was the first nation to issue a sovereign certified climate bond back in 2017, followed by several of its companies. In 2019, Access Bank issued the first Climate Bonds Initiative (CBI)-certified corporate green bond in Africa, raising N15.0 billion. The 5-year, 15.50% fixed rate bond was fully subscribed. The same year, North South Power Company, through the NSP-SPV PowerCorp PLC, issued its Series 1 N8.5 billion Green Bond, which was the first certified corporate green bond and the longest tenured (15 years) corporate bond issued in the Nigerian debt capital markets approved by the SEC. Lagos State is about to become the first issuer of a subnational green bond in Nigeria as it seeks to diversify its financing sources and support sustainable development across the state. On September 10th, its national long-term rating was upgraded to AAA by Fitch Ratings, while its LTR, STR and local currency long-term issuer default ratings were affirmed B.

Read more »

Globeleq completes ZAR 5.2bn refinancing for 238 MW in South Africa

Globeleq has announced the completion of a ZAR 5.2 billion debt financing package for three of its renewable energy facilities in South Africa: the 138 MW Jeffreys Bay Wind Farm, and the 50 MW De Aar Solar and 50 MW Droogfontein Solar plants. The transaction falls under the Department of Mineral Resources and Energy’s (DMRE) Independent Power Producer Office (IPPO) Refinancing Protocol initiated in June 2020. The initiative works on a voluntary basis and targets IPPs from Bid Windows 1 to 3.5 of South Africa’s Renewable Energy Independent Power Procurement Programme (REIPPP). The initiative can include a wide range of options such as maintaining existing debt levels and structure but reducing margins; increasing existing debt levels; increasing debt tenor; converting Johannesburg Interbank Average Rate debt to Consumer Price Index debt; replacing reserve accounts with contingent facilities; replacing junior debt with senior debt introducing preference shares; and restructuring existing risk management strategy and hedging policies. Its end goal is to contribute to the lowering of the wholesale price of electricity. It had already resulting in South Africa’s largest infrastructure deal when the 50 MW Bokpoort CSP plant completed its refinancing in late 2020. The transaction had then created more favourable debt terms and effectively reduced the project’s cost of capital. Globeleq’s projects refinancing is the second transaction to be executed under the protocol. New financing structures effectively unlock reduced tariff to Eskom, which in turn directly impacts the cost of electricity for South African consumers. Globeleq’s refinancing operation, for which Absa acted as the mandated lead arranger and sole underwriter, will save ESKOM ZAR 1 billion in tariff reductions across the three assets over the remaining 12-year term of the power purchase agreements (PPAs). Details on REIPPP projects from Window 1 to 4 are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

Dorman Long Engineering eyes expansion after equity investment from Africa Capitalworks

Dorman Long Engineering, one of Nigeria’s leading oilfields equipment, structural steel, marine structures engineering and fabrication company has just secured a significant investment from Africa Capitalworks to support its expansion. Established in Nigeria back in 1949, Dorman Long Engineering has grown to be one of Nigeria’s leading industrial and infrastructure development players, notably by servicing the country’s hydrocarbons industry. It operates three manufacturing facilities in Lagos, including one at its head office at Idi-Oro, a galvanising plant in Agege and a waterfront facility at the Navy Dockyard. It has successfully executed major engineering services works, including onshore flow stations and major structural fabrication and erection, amongst others, for almost all oil majors and energy services companies operating in Nigeria. More recently, it was a contractor on the Anyala & Madu fields development for First E&P, where first oil was achieved in October 2020. Each field is developed with an unmanned conductor supported platform (CSP), a novel drilling and development technology deployed in the Niger Delta by Dorman Long Engineering and its partners. The company is currently a subcontractor on Seplat Energy’s 300 MMscfd ANOH gas plant, for which it is in charge of the fabrication of several components. The project is Nigeria’s biggest ongoing gas infrastructure development at the moment. The fresh investment officialised today will support Dorman Long Engineering’s refurbishment of its equipment and help the company increase its regional footprint, Chairman Timi Austen-Peters told Hawilti. By expanding existing yards, acquiring additional facilities and expanding its service offering, the company notably aims to tap into new industries such as solar and hydropower. The entry of Africa CapitalWorks will notably support the roll out of such plans and is likely to see Dorman Long Engineering taking on more work across Nigeria while it ventures into neighbouring markets. Africa CapitalWorks Holdings (ACW) is a relatively new vehicle, launched by the CapitalWorks Group to target mid-market companies in sub-Saharan Africa. CDC, the UK’s development finance institution, is a cornerstone investor into ACW and invested $40m in the company back in August 2017. The other major investor is South Africa’s Public Investment Corporation (PIC).

Read more »

Moody’s upgrades Angola’s long-term issuer ratings

Moody’s Investors Service had just upgraded the Government of Angola’s foreign and local currency long-term issuer rater from Caa1 to B3 while maintaining a stable outlook for the country. Moody’s upgrade follows the improvement of Angola’s credit profile on the back of stronger governance and better fiscal management. In particular, Moody’s expects a continued improvement in the country’s fiscal metrics and liquidity and funding risks, especially because of higher oil prices and a stable exchange rate with the Kwanza. As a result, Angola’s local currency (LC) and foreign currency (FC) country ceilings have been raised to B1 and B3 from B2 and Caa1 respectively. “Assuming that oil prices remain around $65/barrel this year and next and around $45-65/barrel in the medium term, with a relatively stable kwanza, Moody’s expects the government debt-to-GDP ratio to decline to 95% this year and below 80% in 2023, from 122% in 2020,” Moody’s said in a statement yesterday. The company further expects the debt-to-GDP ratio to approach 60% by 2025 while the debt-to-revenue ratio could fall to around 300% from 586% last year. A positive improvement is notably seen in the country’s liquidity risks. While Angola’s government borrowing requirements rose to almost 18% of GDP in 2020, they are expected to go down to below 10% of GDP in 2021 and 2022. This is notably the result of continued debt restructuring efforts along with fiscal consolidation. Source: MinFin Finally, the country’s external position can now rely on the stabilization of its exchange rate, with the Kwanza relatively stable at AOA 650/USD since the end of 2020 compared with AOA 165/USD at the end of 2017. While the exchange rate’s liberalization has been an eventful journey, the currency is stabilizing as oil prices recover, which in turns improves Angola’s external position. “Moody’s expects the current account surplus to exceed 5% of GDP in 2021 and to remain in surplus in the coming years. This is explained in part by the rebound in oil prices but also by the structural reduction in the import bill,” explains.

Read more »

Gabon adopts green finance to consolidate bases for sustainable development

The Gabonese authorities intend to step up their action to improve the living environment with a particular emphasis on reducing industrial pollution and safeguarding the biodiversity of its now famous ecosystems. Aware of these challenges of sustainable development and of the transition from a “brown” economy to a “green” economy, the government is resolutely committed to a budgeting process with the objective of consolidating the bases of sustainable development. This new development approach takes into account pre-existing environmental commitments, including a 50% reduction in greenhouse gas emissions by 2025 as well as the preservation of 98% of Gabon’s tropical forests. Renewable energy sources are another important way for the government to reduce emissions and boost growth. Investing in these and other green industries, such as the sustainable development of the fisheries sector, could be the key to bridging the gap between GDP per capita and the poverty rate in Gabon, but also to support sustainable and inclusive development. Within this framework, “sustainable agriculture, sustainable fishing, renewable energy, and eco-tourism can create jobs that tackle the fundamental humanitarian challenges of food scarcity and accessibility to energy,” the government argues in its recently-published National Integrated Financing Framework (CNFI). In practice, these actions relate mainly to the implementation of a green tax framework. They involve, for example, an analysis of public finances (taxation and expenditure), in connection with the green economy, an identification of options to strengthen the links between green levies (existing and future ones) and the use of “green” taxes, as well as the dialogue around the reform proposals necessary for the establishment of a green tax framework. This last point consists of incentives for investments, intended to mitigate greenhouse gas emissions or reduce energy consumption, as well as taxes on CO2 emissions and on the use of energy-intensive technologies. A study is also planned on the scale and parafiscal mechanisms, as well as their impact on the development of the green and blue economic sectors. The government is also counting on a strategic and ambitious approach to mobilize climate finance from the Green Climate Fund (GCF) at scale. This approach should carry out a thorough assessment of the main constraints (financial, technical, legal, capacity and governance). It will also involve updating the climate investment plan (PIC) to develop 79 strategic portfolios of concrete and bankable projects to mobilize funding. Added to this is capacity building to meet financial standards, environmental and social safeguards and gender of the GCF; the identification and incorporation of institutional bridges between the different measures and approaches existing in Gabon related to climate and the environment as well as advocacy to strengthen the regional dimension of GCF projects concerning the Congo Basin. The establishment of a carbon market to monetize the country’s net carbon sequestration is also planned. Just like that of an accounting of natural capital with the evaluation of the ecosystem services provided by the country to the planet as well as the launch of a plea for the integration of natural capital in Gabon’s national accounts, in order to increase GDP while decreasing the debt-to-GDP ratio.

Read more »

The U.S. commits $550m to boost Senegal’s electricity sector

On September 9, the U.S. Government’s Millennium Challenge Corporation (MCC) officially launched the $550 million MCC–Senegal Power Compact in Dakar. The five-year partnership had been signed since 2018 and will be completed by an additional $50 million commitment from the Government of Senegal. Investments will be made specifically in the strengthening of electricity networks in Dakar along with the boosting of electricity access in peri-urban and rural areas of the south and central regions. “The compact investment is designed to strengthen the power sector, by increasing reliability and access to electricity and aims to help the Government of Senegal establish a modern and efficient foundation upon which the nation’s power system can grow,” the MCC explains. The compact includes in fact three distinct projects: a $376.8m project to modernize and strengthen Senelec’s transmission network, a $57.3m project to increase access to electricity in rural and peri-urban areas, and a $43.5m reform and capacity building project to strengthen the country’s laws, policies and regulations governing the electricity sector. The strengthening of the state-utility’s transmission network will mobilise most of the company’s financing and target high-voltage transmission network in around around greater Dakar. It is notably expecting to pave the way for additional private sector investment in power generation in the future, including gas-to-power and renewable energy sources. Beyond official support from the American government, Senegal has attracted several private American investors into its power sector. The 86.6 MW Cap des Biches power plant for instance was the result of an agreement between ContourGlobal and Senelec executed during the Africa Leaders’ Summit convened by President Barack Obama in 2014. Both companies worked to rehabilitate the former GTI Dakar power station and construct a new thermal facility that remains until today one of Senegal’s top performing power plants.

Read more »

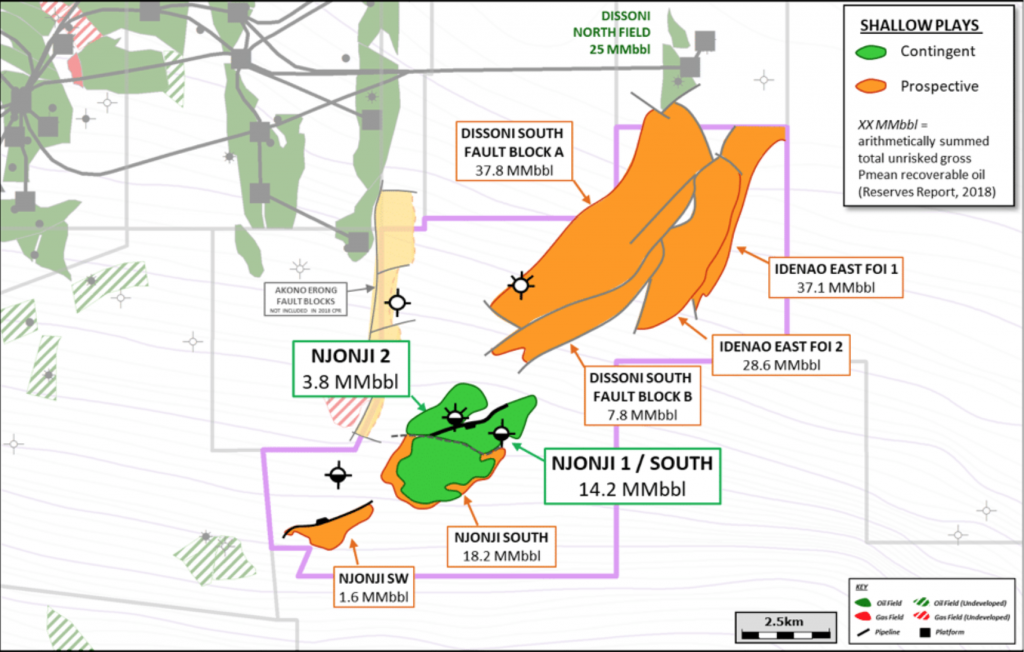

Nigerian trader farms into Thali PSC offshoreCameroun

Private Nigerian trading house Beluga Energy has signed a binding Heads of Agreement with Tower Resources Cameroon last month to acquire a 49% non-operating working interest in the Thali production sharing contract (PSC) offshore Cameroon. As operator, Tower Resources had been looking for a partner for some time in order to drill the NJOM-3 well. Consequently, the farm-out with Beluga Energy covers $15 million towards the cost of that well. With gross mean prospective resources of 111 million barrels across four identified prospects, the Thali PSC could be Cameroon’s next significant shallow water development and sees Beluga Energy entering in a drill-ready asset. Tower Resources has been operating the licence since 2015, when it acquired the block where French major Total had declared two gas discoveries: Rumpi-1 and Njonji-2 (now NJOM-2) and one oil discovery: Njonji-1 (now NJOM-1). Following a reprocessing of all available data, Tower Resouces started planning the drilling of NJOM-3 very early on. However, plans were delayed due first to the lack of site survey data, which was completed and acquired in early 2020, then by the Covid-19 pandemic. Two extensions of the initial exploration periods have provided enough time to drill and complete the well. The last exploration extension period was granted in May 2021 and runs until May 11th, 2022.

Read more »

Kenya is positioning itself as Africa’s next big financial hub

Kenya’s capital, Nairobi, has successfully established itself as a regional hub for trade, commerce, innovation and technology. Now, it wants to compete with Mauritius or even Dubai to be Africa’s new financial hub, positioning itself as a global gateway for capital flowing into Africa’s rapidly growing economies. The country launched this year the Nairobi International Financial Center (NIFC) to deepen Africa’s financial sector, with a target of raising $2bn in investments by 2030. The project has been in the making since 2014 and joins a series of ambitious Kenyan ventures supporting the country’s competitiveness, including the Konza Technopolis. The project received a major boost last July during Kenyan President Uhuru Kenyatta’s visit to the United Kingdom. The visit resulted in the announcement of GBP 132m of UK investment into Kenya and marked the official launch of the NIFC in formal partnership with the City of London. British insurer Prudential notably submitted its application to be the first company to set up in the NIFC while Kenyan mining company Mayflower Gold announced plans to dual list its shares on both the London and Nairobi Stock Exchanges in a deal worth £14 million. The deal ALSO includes closer links between the London and Nairobi stock exchanges, as well as moves to ease incorporation and registration of companies in Kenya. While Kenya’s capital markets are relatively developed, the country’s businesses and economy at large still relies massively on commercial debt from banks. The launch of the NIFC is seen as an additional mechanism to promote the Nairobi Stock Exchange while contributing to the deepening of the region’s capital markets.

Read more »

In 6 Months, Benin Has Raised Over 10% of its GDP in Eurobonds

In January, Benin had kicked off Africa’s financial year with a historic €1bn Eurobond issuance split in two tranches. In July, it continued to tap global capital markets and became Africa’s first nation to issue an SDG-link Eurobond that raised another €500m. In total, the small country of 12m people, often overshadowed by its big neighbour Nigeria, managed to raise a historic €1.5bn, representing over 10% of its GDP. A Well Executed Fundraising Programme At the start of the year, Benin already made headlines with its double issuance of €700m (11-year tenor) and €300m (31-year tenor), which it raised at rates of only 4.875% and 6.875% respectively. Both issuances were massively oversubscribed by 300% and mobilized a total of €3bn, demonstrating significant appetite from global investors for Africa’s debt, even that of smaller and often under-estimated nations. While smaller, the €500m issuance of July is nonetheless historic because it represents Africa’s first Eurobond dedicated to the financing of projects linked to the Sustainable Development Goals (SDGs). Once again, it was massively oversubscribed and mobilized a total of €1.2bn. The bond has a very good rate of 5.25% and a tenor of 12.5 years. Benin Builds Investors’ Confidence Shortly after the January issuance, Fitch Ratings revised the outlook on Benin’s long-term foreign-currency Issuer Default Rating (IDR) from stable to positive and affirmed the IDR at ‘B’. Moody’s Investor Service followed in March by upgrading the Government of Benin’s long-term issuer and senior unsecured debt ratings from B2 to B1. Both upgrades were made on the back of strong fiscal consolidation track record, recognized efforts in debt restructuring and rising economic resilience. Benin remains one of Africa’s fastest-growing economies with GDP growth projected at 5% by the IMF this year, and at 5.6% by Fitch Ratings. The medium-term growth prospects are event better with a projected GDP growth rate of over 6% a year over the 2022-2026 period (IMF). What are the Pitfalls? Benin’s latest issuance shows a growing recognition of the benefits of sustainable borrowing from African governments. While Nigeria had been the first African market to issue a sovereign green bond back in 2017, no African nation had yet issued an SDG-link Eurobond. But overall, the country’s Eurobond borrowing strategy also reflects Africa’s growing appetite for external and foreign-currency debt, supported by interest rates often more attractive than on the domestic market. While several countries have seen the debt-to-GDP ratios soar in recent years, Benin’s outstanding public debt is only at about 46.1% of GDP according to 2020 data from the African Development Bank (AfDB). It is expected to average 40.9% of GDP over 2021–22, well below the 70% threshold set by the West African Economic and Monetary Union. As a result, the risk of debt distress remains moderate in the short-term, providing Benin continues to strengthen its domestic resources mobilization, broaden its tax base and diversify its sources of revenue. African markets have raised a significant amount of foreign-currency debt this year. Beside Benin, Côte d’Ivoire notably issued a €850m Eurobond in February (4.3%, 12-year) while Kenya raised $1bn in June by issuing a 12-year Eurobond at 6.3%. All these issuances were massively oversubscribed, further signaling investors’ confidence in the continent’s growth prospects. The last few months of the year will tell if other countries are able to surf on the same wave or not: on October 11th, Nigeria is notably tapping global markets with a Eurobond issuance expected to raise up to $3bn.

Read more »

Amethis successfully exits Burkina Faso’s leading LPG distributor

Following its investment in Burkina Faso’s leading LPG distributor Sodigaz APC in 2017, Amethis has just sold its 22% stake in the company to African Infrastructure Investment Managers (AIIM). Over the years, Sodigaz has built a 60% market share of Burkina Faso’s LPG distribution market and currently relies on a network of 2,200 gas resellers. Since its beginning in 1977, the company has grown to a 780-employee structure known for its commitment to gender equality. The entry of AIIM into Sodigaz’ capital takes place as West Africa’s LPG market experiences significant growth. As a result, the company has recorded an annual growth rate of over 14% over the past four years and expanded into neighbouring countries such as Benin. As West Africa’s middle class expands and governments seek to fight deforestation and promote public health, the demand for a clean cooking fuel such as LPG is on the rise. This is a trend that applies to the rest of the region and is increasingly generating the interest of investors, especially private equity players. Earlier this year for instance, Investisseurs & Partenaires’ fund I&P Afrique Entrepreneurs 2 made a $3m equity investment in XpressGas, Ghana’s fastest growing LPG distributor.

Read more »