Natural Gas

The US is contemplating increasing debt provided to South Africa’s leading gas, LNG, and helium project

The United States’ International Development Finance Corporation (DFC) is evaluating an increase of its loan to Renergen’s Virginia Gas Project in South Africa by up to $500m. The development finance institution (DFI), previously known as Overseas Private Investment Corporation (OPIC), had already provided $40m in debt to finance Phase 1 of the project. Its growing appetite is welcomed news as most gas infrastructure developers in Africa have criticized the withdrawal of Western DFIs from financing oil and natural gas projects on the continent. South Africa’s first LNG and helium project The Virginia Gas Project is developed by Tetra4, a wholly owned subsidiary of ASX-listed Renergen. It is developing South Africa’s first and only onshore petroleum production right to produce liquefied natural gas (LNG) and helium, a first in the country. Its Phase 1 includes a scalable gas plant and 52km of pipeline, and a maximum production target of 74.6 million cubic feet per day (MMcf/d) (about 350kg) of liquid helium and 2,700 GJ (50 tons) of LNG. Upon start of production, Renergen will notably become South Africa’s first distributor of LNG at filling stations through its partnership with French major TotalEnergies. Phase 2 is expected to follow by 2024, further increasing LNG production to meet an anticipated increase in demand and provide LNG supplies across all major highways in South Africa. Key contracts for phase 2 were awarded in early 2021, including the FEED studies, and the final investment decision (FID) is expected to be taken once these are completed. Phase 2 is designed to allow Renergen to produce significantly larger quantities of LNG and liquid helium: it should notably require a CAPEX of $800m and involve a drilling campaign of 297 wells, anticipated to build up to 44 MMscfd at full production. 65% of Phase 2’s anticipated production is already pre-sold to clients including Linde, Meser, Helium 24 and iSi. Details on the Virginia Gas Project, including contractors, financiers, and offtakers, are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

Nigerian companies team up to provide gas to West Africa’s leading industrial hub

The Lagos Free Zone (LFZ) has officially signed earlier today a Gas Infrastructure Development Agreement with Optimera Energy FZE to develop its own gas distribution network. The new project gathers some of Nigeria’s leading gas players around a new venture committed to promoting gas-based industrialisation. West Africa’s leading industrial hub needs gas Located on the Lekki Corridor, the Lagos Free Zone covers some 830ha and is quickly emerging as West Africa’s leading integrated multi-cluster industrial zone. The project is promoted by the Tolaram Group of Singapore and is co-located with the Lekki Port, Nigeria’s deepest multi-purpose seaport, expected to be completed this year. LFZ has already been successful in attracting several industrial companies and manufacturers including TG Arla, Kellogg’s, Colgate, BASF, Saba Building Systems, or Raffles Oil amongst others. As the zone grows, it seeks to cater for potential high-growth sectors such as FMCG, pharmaceuticals, chemicals, engineering, non-metallic minerals, logistics and mixed-use. This is in return increasing the need to provide world-class infrastructure, including a reliable energy supply. Optimera Energy is now in charge of building, owning, and operating the natural gas distribution network within the free zone. The project is expected to require some $20-25m, with uninterrupted deliveries of piped gas expected to start in 2024. Initial capacity will be set at 5 MMscf/d before being gradually increased to 40 MMscf/d as demand in the zone picks up. The special purpose vehicle (SPV) gathers three of Nigeria’s strongest gas players including natural gas distributor Falcon Corporation Ltd and independent oil & gas companies ND Western and First Hydrocarbon Nigeria (FHN) via their respective subsidiaries ND Western Midstream Ltd and FHN Gas Ltd. “The Optimera consortium is made up of like-minded shareholders who are passionate about a common goal: accelerating the further growth of domestic gas utilisation in Nigeria. Having reliable dedicated gas supply infrastructure installed in the LFZ adds tremendous value to existing industrial concerns and will increase the Zone’s attractiveness to future customers.” Audrey Joe-Ezigbo, Managing Director of Optimera Energy and Deputy Managing Director of Falcon Corporation. Promoters of gas-based industrialisation Falcon Corporation has been successfully operating the Ikorodu natural gas franchise in Lagos since November 2006 and will bring its experience in building and operating gas pipeline networks for industries. The company is also a bulk distributor of Liquefied Petroleum Gas (LPG) in the domestic market and is actively developing LPG bulk storage infrastructure in the Niger Delta. On the other side, both ND Western and FHN are amongst Nigeria’s biggest gas producers from OML 34 and OML 26 in the Niger Delta, with combined gas reserves of over 4 Tcf. Via Optimera Energy, they will be transporting their gas to the Lagos Free Zone via the Escravos-Lagos Pipeline System (ELPS). ND Western has notably increasingly positioned itself as an enabler of industrialisation in Nigeria. The company already supplies gas to several power plants in the country via ELPS and exports gas to West African markets via the West Africa Gas Pipeline (WAGP). On OML 34, it has recently embarked on the development of an industrial park providing industries with direct access to cheaper gas directly at the pump. The rise of gas-to-industry in Nigeria Because the power sector remains illiquid, the promotion of gas utilization across other industries is seen as a priority under Nigeria’s Decade of Gas initiative. Chief amongst them is the expansion of the downstream gas sector, especially Autogas for cars and piped natural gas (PNG) for industries. Consequently, industrial gas off-takers are on the rise, and the volumes of domestic gas monetised by Nigerian industries (gas-to-industry) have doubled between 2015 and 2021. To know more about the trends, actors, and projects shaping up Nigeria’s natural gas sector, please log into your Hawilti+ research terminal at plus.hawilti.com.

Read more »

Sasol launches $5m CNG fund with Mozambique’s National Investment Bank (BNI)

To support gas monetization in Mozambique, Sasol has signed today an agreement with the country’s National Investment Bank (BNI) and the Ministry of Mineral Resources and Energy to set up a $5m fund for the development and expansion of compressed natural gas (CNG) projects. The fund will be financed by Sasol and managed by BNI and open to any individuals or SMEs seeking to convert to gas. “The CNG Credit Line offers special conditions for those interested in converting their vehicles to natural gas, and for retailers wishing to equip their fuel stations with CNG refuelling units,” Sasol said. Sasol is notably expecting the credit line to benefit public transport operators seeking to decrease their reliance on diesel at a time when soaring global prices put pressure on net importers like Mozambique.

Read more »

Hawilti launches gas research programme on Nigeria

Hawilti has marked the launch of its gas research programme on Nigeria with the release of a comprehensive investment report on the country’s natural gas sector earlier this week. The 2022-2023 programme seeks to analyse the growth of Nigeria’s natural gas value-chain in light of current regional and global market dynamics. While the Nigerian government had already been pushing for a stronger adoption of gas domestically, the war in Ukraine has repositioned Nigeria as a strong potential gas supplier for the export market as well. Long-stalled projects such as Brass LNG or the Nigeria-Morocco Gas Pipeline (NMGP) could benefit from renewed interest in exporting African gas. Meanwhile, the need to secure energy for Nigerian households and industries, especially in a context of soaring diesel prices, is putting pressure on the country’s gas value-chain to provide alternative solutions such as compressed natural gas (CNG), liquefied natural gas (LNG), liquefied petroleum gas (LPG) and piped natural gas (PNG). To address those challenges, Nigeria has chosen gas as its key transition fuel and named the 2020-2030 period as “Decade of Gas” in a bid to monetize its 206 Tcf of gas reserves to drive industrialization, create jobs, and generate revenue. This is in turn generating increased interests from local and foreign investors seeking to invest in the country. While little confidence exists in the strength of Nigeria’s domestic gas value-chain, long-term industry fundamentals support a strong case for investing into the country’s gas production and infrastructure. Hawilti’s research programme is developing new data sets and perspectives into the Nigerian market, focusing on private sector-led initiatives and projects across the exploration & production and midstream segments, while highlighting the growth potential of key commodities such as LPG, LNG, and CNG. All market information generated as part of the programme is now available on the Hawilti+ research programme and to Hawilti subscribers and partners. In addition, Hawilti will be expanding its suite of quarterly sector watch on the country’s LPG and small-scale LNG industries, while releasing a new comprehensive investment report twice a year.

Read more »

Worley awarded FEED Phase II contract for Nigeria-Morocco Gas Pipeline

Worley has announced that it has been awarded a contract to provide main front-end engineering design (FEED Phase II) services for the 7,000km Nigeria-Morocco Gas Pipeline (NMGP) project. The feasibility study and FEED Phase I were previously completed by Penspen. The project is led by Morocco and Nigeria’s national oil companies, the Office National des Hydrocarbures et des Mines (ONHYM) and NNPC Ltd. If completed, it would be the longest offshore pipeline in the world. Its FEED study already received financing from the Islamic Development Bank in December 2021. The development bank had then declared that a final investment decision (FID) was targeted for 2023. The pipeline has been on the table for some time and is seen as an extension of the existing West Africa Gas Pipeline (WAGP) that was commissioned in 2011. However, WAGP has been plagued by several operational issues, including unreliable gas supplies from Nigeria and legacy debt payments from off-takers. The NMGP is expected to traverse 13 West African countries and offer African gas producers a new avenue to export their gas to neighboring countries and to Europe. Nigeria, Ghana, Côte d’Ivoire, Senegal, and Mauritania all have discovered gas reserves located offshore. Gas deliveries could be made across the pipeline route to African markets seeking to secure additional gas supplies or exported all the way up to Europe via Morocco. “The overall FEED services will be managed by Intecsea BV, our offshore engineering consultancy business in The Hague, the Netherlands. This includes the development of the project implementation framework and supervision of the engineering survey,” Worley said in a statement. Nigeria holds Africa’s largest gas reserves and is increasingly seeking to monetise it domestically and for exports. On February 16th, Minister of Petroleum Timipre Sylva was in Niger to sign the Niamey Declaration with his counterparts from Algeria and Niger. The agreement seeks to put the Trans-Sahara Gas Pipeline (TSGP) Project back on track – another gas pipeline that would allow Nigeria to export its gas to Europe via Niger and Algeria. Earlier this month, Minister Timipre Sylva also expressed interest in reviving the Brass LNG export terminal project – a 10 mtpa LNG export scheme first discussed in 2003.

Read more »

Invictus Energy commits to more gas exploration onshore Zimbabwe

Geo Associates, who is about to drill in Zimbabwe what is believed to be the largest undrilled structure onshore Africa, has just committed to a second well this year. The company is a subsidiary of Australian independent Invictus Energy and holds an 80% interest in SG 4571 over the Cabora Bassa Basin in northern Zimbabwe. The area had already been explored by Mobil back in the 1990s, when the American major spent $30m acquiring surface and subsurface data, including gravity surveys and over 1,600 line kilometres of 2D seismic data. Back then, the massive 200km2 Mzarabani anticline had been identified and mapped, believed to host a conventional gas target. Last year, Polaris Natural Resources acquired 402.2km of 2D seismic over the license to support exploratory drilling by Exalo Drilling in June this year. The Mzarabani Prospect alone is estimated to contain 8.2 Tcf of gas and 250 million barrels of conventional gas / condensate (gross mean unrisked) across 5 horizons. But Geo Associates has decided to bet even higher on Cabora Bassa and has just signed a Heads of Agreement with the Sovereign Wealth Fund of Zimbabwe (SWFZ) to amalgamate SG 4571 with SWFZ’s MSC003 Cabora Bassa South Reserved Area. As a result the licence area has increased sevenfold from 100,000 ha to 709,300ha andnow covers the entire Cabora Bassa Basin in Zimbabwe. The company notably committed to increase its minimum work programme obligations for SG 4571’s second exploration period, which runs to June 2024. These include the acquisition of an additional 400km line of seismic data in the expanded area, and the drill of a second exploration well as part of the drilling campaign set to start in the middle of this year. Full details on the Cabora Bassa Gas Project onshore Zimbabwe are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

World’s second largest granulated urea plant commissioned in Nigeria

Yesterday, President Muhammadu Buhari commissioned Africa’s largest granulated urea plant and the second biggest in the world in Ibeju Lekki. The Dangote Fertilizer facility has a capacity of 3 million tonnes per annum (mtpa) and is now making Nigeria self-sufficient in fertilizers, with extra capacity reserved for exports. “We have already started exporting to the USA, Brazil, India and Mexico,” Aliko Dangote said during the commissioning ceremony held at the Lekki Free Zone. The $2.5bn twin train facility processes domestic gas to produce urea and ammonia, and is located next to the 650,000 bpd Dangote refinery and petrochemicals complex, where operations are yet to start. Just this month, state-owned NNPC, the Shell Petroleum Development Co. (SPDC) JV and Dangote sealed a new Gas Supply & Aggregation Agreement (GSAA) to supply 70 MMscfd of gas from the Tunu CPF (OML 35) to Dangote Fertilizer. Another GSAA had previously been signed in December 2019 with Chevron Nigeria.

Read more »

OML 113 transferred to new operating vehicle as partners prepare for gas redevelopment offshore Lagos

After two years of delay, the Nigerian authorities have finally approved PetroNor’s acquisition of Panoro Energy’s subsidiaries in Nigeria, Pan-Petroleum Services Holding BV and Pan-Petroleum Nigeria Holding. The deal was initially inked in October 2019 and had been awaiting government consent since then. Through this acquisition, PetroNor is acquiring Pan Petroleum Aje Ltd, which holds a 6.502% participating interest and 16.255% cost bearing interest in OML 113. This represents a total economic interest of 12.1913% in the license that contains the Aje field offshore Lagos, which produced oil from 2016 to 2021 via the Tamara Nanaye FPSO. Source: DRPC/NUPRC Along with the completion of the acquisition, the Nigeria Upstream Petroleum Regulatory Commission (NUPRC) has also given consent for the transfer of OML 113 to Aje Petroleum AS, a special purpose vehicle owned by Yinka Folawiyo Petroleum (YFP, 55%) and PetroNor (45%). Under the deal, PetroNor will serve as the new technical operator for the redevelopment of Aje into a gas project, on behalf of YFP. The Field Development Plan (FDP) for the new Turonian Aje gas project on OML 113 aims at increasing production to 15,000 barrels of oil equivalent per day (boepd) via the drilling of two new gas producers and one oil producer. It is notably being planned along with the replacement of the Tamara Nanaye FPSO with a new unit able to process increased liquids production and up to 110 MMscfd of gas. This new FPSO could even become a regional field center since it is located around substantial proven resources such as Albian but especially Ogo, a world-class discovery on the neighbouring OPL 310 operated by Optimum Petroleum. The latest plans available had a projected production peak of 26,000 boepd in 2025, with most incremental production being made of gas reserved for power generation and exports through the nearby West Africa Gas Pipeline (WAGP), or supporting LNG production. The partners have set OPEX at about $30m a year, including FPSO bareboat, Operation & Maintenance and G&A. The project is currently at FEED stage and is expecting FID in 2022 at the earliest. Meanwhile, the Tamara Nanaye FPSO stopped producing from the Aje field in November 2021. Hawilti reported earlier this year on its research terminal that the vessel is being refurbished before redeployment at the Kalaekule field on OML 72. It will continue to be operated and maintained by Nigerian services conglomerate Century Group. Details on the development of OML 113 offshore Lagos are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

Chariot announces significant gas discovery at Anchois-2 offshore Morocco

AIM-listed Chariot has confirmed the presence of significant gas accumulations in the appraisal and exploration objectives of its Anchois-2 well within its Lixius License offshore Morocco. Preliminary interpretation of the data has identified a calculated net gas pay totaling over 100m (compared with 55m at Anchois-1). At Anchois-2’s appraisal target, a continuation of a reservoir drilled by Anchois-1, the Gas Sand B notably has a calculated total net gas pay of over 50m in two stacked reservoirs of similar thickness. At the well’s exploration targets, Gas Sands C, M and O were successfully encountered with multiple gas-bearing intervals, Chariot has said. This new significant gas discovery will help to expand the Anchois gas field and possibly expand the scale of its gas development in the future. It also significantly de-risks additional exploration prospects within the license area. Chariot has been operator of the Lixius License since 2019 with a 75% interest. The block was previously known as the Tanger-Larache permit and already included the Anchois-1 discovery made by Repsol in 2009. Anchois’s first phase of development is expected to include the drilling of four production wells tied into a subsea manifold, along with the installation of a 14in-diameter, 40km subsea flowline with control umbilical to the subsea manifold, construction of a 53 MMscfd onshore central processing facility (CPF) for exporting gas, and a 14in-diameter onshore pipeline for gas export. In October 2021, Chariot signed a Memorandum of Understanding (MoU) with a leading international energy group agreeing on the key terms of gas offtake from Anchois. Under the Mou, the key terms of the future gas sales agreements will be for c.40 MMscfd, for up to 20 years on a take or pay basis. The phase two development plan is expected to involve additional wells to tie-in the Anchois W, Anchois WSW and Anchois SW areas of the field into the subsea manifold. It will be financed using the cashflow generated from first phase production. Details on the Anchois Gas Development are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

Chariot starts drilling offshore at Morocco’s flagship gas project

Chariot has announced today the commencement of drilling operations at its Lixus license offshore Morocco. The campaign will drill and complete the Anchois-2 gas appraisal and exploration well and re-enter the previously drilled Anchois-1 gas discovery well, with a view of fast-tracking the offshore gas development of Anchois. The Stena Don drilling rig is mobilized to carry out drilling operations. The Anchois gas field lies in water depths of 850m and was first discovered in 2009 by former operator Repsol. The field was then transferred to Chariot when the company was awarded the Lixius Offshore Licence in 2019. Back then, the Anchois-1 gas discovery had 307 billion cubic feet (Bcf) of 2C contingent resources offering near-term development opportunity and had identified a deeper potential not penetrated by the Anchois-1 well of 116 Bcf 2U prospective resource. Under the new licence’s commitment, Chariot reprocessed existing data which led to upgrading the total remaining recoverable resource to well over 1 trillion cubic feet (Tcf) of gas in 2020. Ongoing activities now target a final investment decision (FID) in 2022 to achieve first gas by 2024 with a production rate of 53 million standard cubic feet per day (MMscfd). Estimated capex required to bring the development online are currently anticipated to be in the region of $300-500m.

Read more »

Tanzania: ORCA Energy submits $50m capex plan for Songo Songo development next year

The ORCA Energy Group has planned a $50m capex for the continued development of the Songo Songo gas project in Tanzania next year. Via its subsidiary PanAfrican Energy, ORCA operates the wells and gas processing plant at the Songo Songo island in central Tanzania. The 2022 programme includes $20 million for a 200 km2 3D seismic program over the Songo Songo development license, $11.5 million to expand the PanAfrican Energy’s existing downstream gas and CNG distribution system, and approximately $7 million for ongoing maintenance and facilities projects. The remaining $11.5 million represents the expenditures associated with the current work over program and inlet compression project, representing a combined $63m investment approved in 2019. The seismic programme would be pretty significant because PanAfrican Energy currently relies on 2D seismic lines ranging from 1978 to 2009. These are insufficient to maximise future upstream gas developments at Songo Songo. “The 3D seismic program is required to de-risk both the future development drilling in the SS gas field and potential exploration drilling of prospective resources prior to the SS license expiring in October 2026.,” ORCA said last week. Source: ORCA Energy Group ORCA continues to see potential for growth and gas production at Songo Songo, even beyond 2026. For now, it is projecting a gas production of at least 100 MMsfd for 2022, including about 40 MMcfd of Protected Gas reserves for the Tanzania Petroleum Development Corp. (TPDC). Details on the Songo Songo Integrated Gas Development are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

Nigeria: 188 MW Aba Integrated Gas-to-Power Project gets $50m boost from Afreximbank

Last week during the second Intra-African Trade Fair in Durban, the African Export-Import Bank (Afreximbank) signed a $50m term loan facility with Geometric Power Limited for its Aba Integrated Power Project in Nigeria. The facility will notably help finance the initial capital required to acquire rights to the Aba Ring Fenced Area within which electricity from the power plant will be distributed and sold. It will also support the completion of remaining works, and the commissioning and commencement of operations of the project. A Unique and Fully Integrated Gas-to-Power Project The Aba IPP has been in the making for quite some time and will be Nigeria’s first integrated and independent power utility. The project includes a 141 MW gas-fired power plant (licensed for 188 MW), a 27km gas pipeline, and a distribution utility selling power within a ring-fenced distribution network. The project is structured as an embedded electricity facility designed to generate and distribute its own electricity. Electricity will be generated by Geometric Power Aba Limited (GPAL), the entity that owns and operates the power station, but will be distributed by Aba Power Limited Electric (APLE). The former has a power generation license while the latter benefits from an electric distribution license. Gas feedstock will be supplied by the Shell Petroleum Development Co. (SPDC) joint-venture, with whom a gas supply and aggregation agreement (GSAA) was executed in late 2018. The agreement notably covers the supply of about 43 MMscfd of gas. “Being one of the only 24hr reliable power supplier, Aba IPP will revive moribund industries, power the Enyimba Economic City as well as markets such as the famous Ariaria International Market,” declared Geometric Power Chairman & CEO Prof. Bart Nnaji, who previously served as Nigeria’s Power Minister in 2011 and 2012.

Read more »

Invictus Energy completes 2D seismic over Cabora Bassa onshore Zimbabwe

Invictus Energy has completed the acquisition of 839.3km of high-resolution 2D seismic data as part of its Cabora Bassa 2021 (CB21) survey onshore Zimbabwe. This significantly exceeds the company’s minimum work programme of 300km of 2D seismic data over its Special Grant 45 71 (SG 4571) license that runs to June 2024. 402.2km of data was acquired over SG 4571, where lies the Muzarabani prospect that Invictus Energy will drill next year. The remaining 437.1km of contiguous data was acquired in an existing application area. “The seismic data processing and interpretation is ongoing and once completed will enable us to identify and mature additional prospects and leads. The better imaging over the giant Muzarabani structure is very encouraging and once the interpretation of the full dataset is completed, we expect to refine the location for the basin opening Muzarabani-1 well which is scheduled to be drilled in 1H 2022,” Invictus Energy Managing Director Scott Macmillan commented. Invictus has an 80% equity stake in SG4571 via its subsidiary Geo Associates (Private) Limited. The license was granted for three years back in August 2017 and is currently in its second exploration period. Details on the Cabora Bassa Project are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

Renergen’s shares take off after 600% increase in reserves at South Africa’s Virginia Gas Project

Renergen’s shares have been up +43.14% on the Australian Securities Exchange (ASX) and +31.27% on the Johannesburg Stock Exchange (JSE) since Friday. The most significant jump happened today with an increase of almost +30% on the ASX and +15% on the JSE after the company reported a 600% increase in its 1P helium reserves in South Africa. Source: Yahoo Finance Renergen is South Africa’s only onshore petroleum production right holder and sits over a Production Right area of 187,000 ha in the Free State around the towns of Welkom, Virginia and Theunissen. This is where its subsidiary Tetra4 is developing methane and helium reserves to produce liquefied natural gas (LNG) and helium, mostly for the domestic market at first. A 600% Jump in 1P Helium Reserves Following the recent successful drilling campaign and as part of Renergen’s ongoing assessment and development of Virginia, the company had commissioned international Reserves and Resources accreditation agency Sproule to estimate its reserves and resources of methane and helium within the Virginia Production Right area as at September 1, 2021. Sproule’s estimation resulted earlier today in an upgrade of both methane and helium reserves. 1P helium reserves have notably increased by an impressive 620% to 7.2Bcf while 1P methane reserves have increased by 427% to 215.1Bcf. As a result, 2P total gas, including methane plus helium, is now equivalent to 65 MMscfd for the remainder of the license tenor. Phase 1 is Almost Complete The development of Phase 1 at Virginia is already well underway and involves the connection of 12 existing gas wells to a new 52km gas pipeline and small-scale LNG and helium processing plant. Renergen secured all the necessary funding for this first phase and held a groundbreaking ceremony at the end of 2019. Drilling is now ongoing, along with pipeline construction and the development of the gas plant, with a commissioning expected before the end of 2021 and start of helium production in Q1 2022. Meanwhile, logistics and transport companies are expected to make a major part of future customers, and Renergen launched South Africa’s first LNG auction in July 2020 to allocate future LNG production. Strong interest for the auction confirmed the appetite of the South African market for cleaner and cheaper fuels. In August 2021, Renergen also executed its first LNG supply agreement not linked to the transport sector: the 5-year contract was inked with Consol Gloss for about 14 tons per day of LNG and will start in January 2022. It carries a price which will be linked to the floating LPG price in South Africa. Towards Phase 2 Phase 2 is expected to follow by 2024, further increasing LNG production to meet an anticipated increase in demand and provide LNG supplies across all major highways in South Africa. Key contracts for phase 2 were awarded in early 2021, including the FEED studies, and the final investment decision (FID) is expected to be taken once these are completed. Phase 2 is designed to allow Renergen to produce significantly larger quantities of LNG and liquid helium with a target of 44 MMscfd of gross gas sales made up of helium and methane. Phase 2 is expected to require a CAPEX of $800m and involve a drilling campaign of 297 wells, anticipated to build up to 44 MMscfd at full production. 65% of Phase 2’s anticipated production is already pre-sold to clients including Linde, Meser, Helium 24 and iSi. Details on the Virginia Gas Project are available in the “Projects” section within your Hawilti+ research terminal.

Read more »

Gabon exposes clear vision on what to do with its natural gas

Gabon is thought to hold anywhere between 3 to 5 trillion cubic feet (Tcf) of gas, although the country remains a small gas producer. To date, most of its gas has remained on the ground or flared – with only small quantities monetised domestically for power generation in Libreville and Port Gentil. But as Gabon implements an ambitious “Green Gabon” environmental policy and seeks to diversify its economy, the country wants to cut routine flaring altogether and monetise it for the benefits of its industries, households, and economy. The recent Gabon Oil, Gas & Energy Summit organized by IN-VR in Libreville last October notably exposed the alignment of most parties on the need to monetise gas instead of flaring it. A New Gas Strategy in the Making To achieve its gas ambitions, Gabon is currently working on a new Gas Master Plan with Wood Mackenzie and the World Bank’s Global Gas Flaring Reduction Partnership (GGFR). The plan will have four major ambitions: reduce gas flaring, increase energy security, expand access to affordable energy and attract investments into gas projects. Gabon’s flared gas currently emits about 2,244,500 tonnes of CO2 per year, enough to generate 500 MW of power. Natural gas also features prominently within the country’s 2021-2023 Plan to Accelerate Transformation (PAT), which includes a dedicated Gas Task Force headed by former Gabon Oil executive Yann Pierre A. Livulibutt Yangari. “Our gas strategy is targeting actions across the whole value-chain. In upstream, we want to get operators to explore for gas and stop considering it as a risk. In midstream, we want to see flared gas being monetised for the benefits of the Gabonese economy. Finally in downstream, we want to improve gas supplies especially of liquefied petroleum gas (LPG), compressed natural gas (CNG) and liquefied natural gas (LNG),” Yangari said during IN-VR’s summit. As it stands, Gabon intends to primarily monetise flared gas to generate power, manufacture urea and produce methanol. These are the major industries identified based on existing gas reserves and technology available from existing investors and operators in the country. Once these are developed, hopes are that by-products would follow, especially when it comes to LPG, CNG (Autogas) and micro-LNG. Source: DGEPF “We are working on supporting the development of a gas-based economic network to support local content development, promote technology adoption and support industrialisation,” Yangari added. While Gabon has not discovered enough gas reserves to justify the development of more significant industries like LNG for export or gas-to-liquids, the country remains hopeful. Its 12th Licensing Bid Round has resulted in the award of new exploration blocks, and upcoming drilling campaigns could result in new gas discoveries supporting further gas developments in the medium-term. To justify the investment, Gabon is putting forward its growing industrial base driving demand for both power and gas. Last September, the Gabon Power Company (GPC) notably signed a landmark Concession Agreement with Wärtsilä for the development, supply, construction, operation, and maintenance of a new 120 MW gas-to-power project in Owendo, next to the capital city of Libreville. But beyond just the power sector, Gabon wants to provide gas to its mining, forestry, agro-industry, and steel industries. In parallel, its logistics network is expanding with railways and maritime industries both positioned to be potential off-takers sooner than later. An Opportunity for Small-Scale Gas Projects Gabon’s vision relies on the monetization of gas into CNG for transport and micro-LNG for industries. A key strategy is to expand the country’s CNG network but use micro-LNG for any remote industries located over 400km from producing fields, especially mining industries. To support such expansion, the country is seeking investors across several projects such as LPG plants, LNG and CNG plants, LNG and CNG storage, onsite regasification and bi-fuel conversion. Chief amongst them is the need to secure 30,000 cubic metres of additional butane storage capacity, up from only 4 to 5,000 cubic metres now. Source: DGEPF Port Gentil features prominently within that vision as a pilot city to grow the CNG industry. It is there that Perenco already runs a private gas retail station for 40 of its own vehicles. Now, Gabon wants to grow the market by constructing public CNG stations in partnership with oil marketers and develop a new pricing structure for CNG. The aim is clear: reduce petroleum products imports while generating additional revenues from domestic gas. Perenco Takes the Lead Perenco will be a key actor of that transition to gas. The operator is the country’s sole commercial gas producer and currently supplies gas feedstock to the power stations of Port Gentil and Libreville. In fact, 100% of Port Gentil’s power relies on Perenco’s gas while 70% of Libreville’s power is generated from the operator’s gas supply. “We have invested $500m into the development of a 400km onshore and offshore gas gathering system in Gabon that supplies gas to power plants but also key industries such as Sobraga. In the process, we created 150 jobs,” Director General Adrien Broche said during the IN-VR Summit. Perenco is now increasing its investments and leveraging on its existing infrastructure to commission a 10 to 15,000 tonnes per annum (tpa) LPG plant in Batanga by 2023. Batanga is currently the cornerstone of its gas business and is equipped with enough compressors to compress gas to over 100 bars so it can be transported across the country. “The Libreville and Port Gentil power stations currently represent an off-take of about 40 MMscfd,” Broche explained. “While only half of that capacity was coming from flared gas, we are installing additional compression capacity so all feedstock supplied to power plants comes from previously flared gas. We have installed two onshore compressors this year and are now expecting additional ones for offshore operations. By mid-2022 or early 2023, all gas we send onshore for power generation will come from previously burned resources,” he added. The Need for an Industry and Policy Consensus But to furter monetise gas and create jobs, Gabon must first find a way to aggregate

Read more »

Gabon on the move: what you need to know ahead of the Gabon Oil, Gas & Energy Summit in Libreville this week

Nested in the Gulf of Guinea, Gabon has built itself a reputation of environmental stewardship and sustainable development of its natural resources. The country of less than 2.5m notably hosts Africa’s largest forest elephant population and is covered at 88% by rainforest. Despite being an established offshore hydrocarbons province, Gabon is steadily diversifying away from oil. A public-private partnership with ARISE IIP resulted in the establishment of one of Africa’s most modern and efficient free zones now serving a growing industrial and mining base. The country is in fact one of the world’s top producers of manganese, of which it exported almost 4m tonnes in the first half of the year. Gabon has also successfully industrialised its wood industry to become a recognised exporter of timber: between January and June 2021, the country produced over 1 million m3 of logs. Gabon’s economy remains fairly diversified compared to that of its African neighbours. Its oil & gas sector’s contribution to the GDP stood at 37.7% in 2020 and represented 33% of government revenues last year. Oil exports also accounted for 70% of total export revenues. Maintaining the pace of investment in the country’s hydrocarbons value-chain remains a priority for the government, especially as it seeks to develop gas-based economies and use oil revenues to invest in sustainable infrastructure and the conservation of its environment. A Focus on Reversing Production Decline Gabon is member of the Organisation of Petroleum Exporting Countries (OPEC) and produced an average of 183,000 barrels of oil per day (bopd) between January and September 2021. This makes it sub-Saharan Africa’s fourth largest producer, behind Nigeria, Angola and Congo-Brazzaville and more or less at par with Ghana. Production has been in decline for several years and has stagnated in the recent past. Gabon launched its 12th Licensing Bid Round before Covid19, which it is just concluding now. The round generated relatively strong interest given market dynamics, and award letters started being issued this month with BW Energy provisionally securing two blocks along with partners Panoro Energy and VAALCO Energy. Source: DGEPF The award of new exploration acreage is much needed in order to encourage seismic acquisition and exploratory drilling and ultimately maintain production in the medium-term. Exploration has so far been a miss this year, with BW Energy’s Hibiscus Extension appraisal well (DHIBM-2) encountering water in the first half of the year, and its Hibiscus North exploration well (DHBNM-1) failing to deliver on pre-drill resource estimate in July. An Independents’ Market Gabon is an independents and national oil companies (NOCs)’ game. Shell Gabon sold all its assets in the country to Assala Energy in November 2017, and Total Gabon sold seven of its non-operated mature fields and operatorship of the Cap Lopez Oil Terminal to Perenco in July 2020. Beyond Assala Energy and Perenco, Gabon’s upstream sector is dominated by Maurel & Prom, VAALCO Energy and BW Energy along with a few NOCs such as Petronas. TotalEnergies remains the only IOC still operating upstream assets in the country. Gabon continues to offer significant opportunities for independents, both onshore and offshore. In February 2021, Panoro Energy acquired Tullow Oil’s 10% working interest in BW Energy’s Dussafu Marin Permit. A New Strategy to Monetise Domestic Gas Gabon has been working for a few years on a new strategy to monetise gas to generate additional electricity and develop new gas-based industries. The move benefits from significant political will and support and is one of the key pillars of the country’s new three-year plan over the 2021-2023 period, dubbed Plan to Accelerate the Transformation (PAT). Because Perenco represents most of the country’s operated gas production, it will play a major role in the development of Gabon’s domestic gas market. The company completed this year studies and plans for the new 10,000 metric tonnes Batanga LPG plant, where construction is expected to start before the end of the year. In July 2019, Gabon’s Ministry of Petroleum, Gas and Mines had also signed an agreement giving the Olowi Field to Perenco as its new operator. The field was developed between 2005 and 2018 by Canadian Natural Resources and is now to be redeveloped under an integrated gas project. Source: DGEPF Finally, an expanding gas industry will benefit the power sector. Gabon already runs several gas-to-power facilities and in September 2021, the Gabon Power Company (GPC) signed a landmark Concession Agreement with Wärtsilä for the development, supply, construction, operation, and maintenance of a new 120 MW gas-to-power project in Owendo, next to the capital city of Libreville. A Diversifying Energy Basket Beyond gas, Gabon is also expanding its energy sector with the development of its solar and water resources. Several hydropower plants are currently being developed, When it comes to hydroelectricity, Meridiam and the Gabon Power Company successfully reached financial close on the 35 MW Kinguélé Aval in July this year. Additional facilities include the 15 MW Dibwangui hydropower plant and the 73 MW Ngoulmendjim hydropower plants, whose power purchase agreements (PPA) were signed with Eranove in 2018. Solar energy is also making its entry into the country’s grid with the signing last August of a contract with the Turkish group Desiba Energy for the construction of a 20 MW solar power plant in Doubou, in the province of Ngounié. To find out about investment and business opportunities in Gabon, register for IN-VR’s Gabon Oil, Gas & Energy Summit hybrid conference taking place in Libreville and online between October 20th-22nd. More information at https://www.in-vr.co/gabon. All details on ongoing and future projects across Gabon’s energy sector are available within your Hawilti+ research terminal.

Read more »

Orca Energy to execute $21.4m workover programme in Tanzania

PanAfrican Energy Tanzania, the subsidiary of the Orca Energy Group that operates the wells and gas processing plant at Songo Songo in Tanzania, has signed an agreement with Exalo Drilling for the workover of three onshore wells. Activities are set to start in September 2021 on Songo Songo Island. The 2021 workover programme will notably see the wells recompleted with corrosion resistant chrome tubing while returning two wells to production and ensuring the third well continues to produce safely. Songo Songo is Tanzania’s flagship gas project and currently supplies about 60% of Tanzania’s gas, mostly used for power generation. While PanAfrican Energy operates the wells and the 110 MMscfd gas processing plant, the Songo Songo development remains owned by Songas, itself majority owned by Globeleq. Only gas produced beyond a threshold of 44.8 MMscfd can be freely marketed and sold by PanAfrican Energy. Source: Orca Energy Group The first 45 MMscfd is classified as “Protected Gas” and is owned by the Tanzania Petroleum Development Corp (TPDC) and sold under a 20-year gas agreement expiring on July 31st, 2024. This gas is used by Songas to fuel its 190 MW Ubungo gas-to-power plant but is also used for distribution to the Tanzania Portland Cement Company, and for Tanzania’s village electrification programme. Such distribution is ensured by Songas’ infrastructure which includes the 105 MMscfd, 232km pipeline to Dar es Salam and a 16km spur line to the cement plant. Beyond 44.8MMscfd, the gas is classified as “Additional Gas” and can be freely commercialized by PanAfrican Energy. The company has been steadily increasing its production and sales of Additional Gas to support additional power generation facilities in Dar es Salam, power several industries and develop a growing Compressed Natural Gas (CNG) business.

Read more »

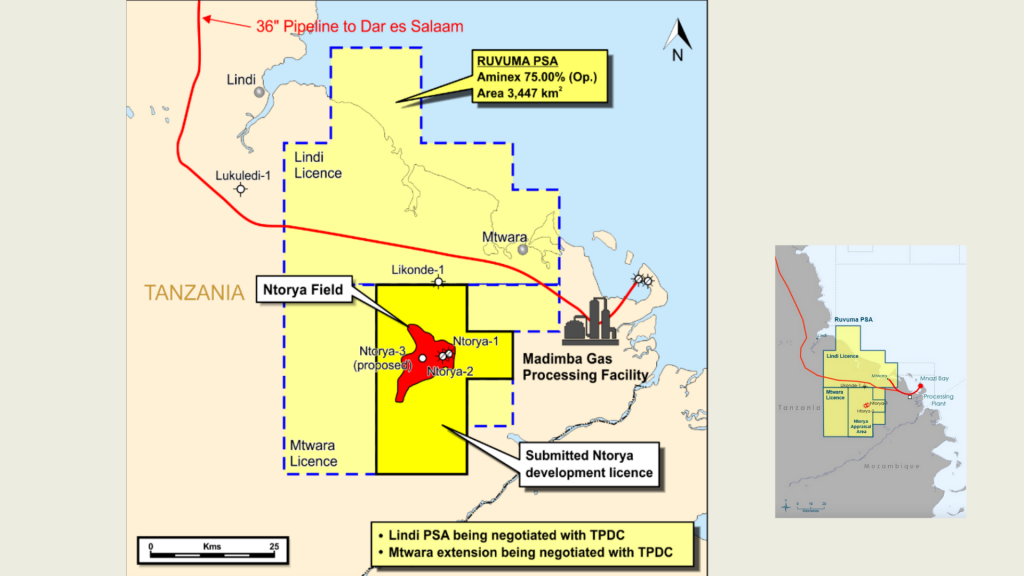

APT receives 2-year extension to meet gas exploration targets onshore Tanzania

ARA Petroleum Tanzania (APT), which took over the operatorship of the onshore Ruvuma PSA in Tanzania last year, has received a two-year extension of the license. The granting of the extension was necessary to complete key exploration activities on the block, including the acquisition of 200 km2 of 3D seismic data and the drilling of the Chikumbi-1 exploration and appraisal well (formerly known as Ntorya-3). Completion of the exploration programme will further support the conclusion of negotiations of the Gas Terms for the Ruvuma PSA and pave the way for the development of the Ntorya Gas Project. The development of the Ntorya gas accumulation has the potential to be Tanzania’s next big domestic gas project. Located in southern Tanzania where Maurel & Prom produces gas from the Mnazi Bay PSC since 2015, Ntorya used to be operated by Aminex’ subsidiary Ndovu Resources with a 75% interest before APT took over operatorship of the asset with a 50% interest last year. Aminex has since then retained a 25% interest in the license. The Ntorya accumulation is located within the onshore Ruvuma Production Sharing Agreement (PSA) signed in October 2005, which contains the Mtwara licence and the Ntorya development area, the latter being currently in negotiation. The PSA was operated by Tullow Oil until 2011 and saw the successful drilling of the Likonde-1 well in 2010, the Ntorya-1 well in 2012 and the Ntorya-2 well in 2017. Both Ntorya-1 and Ntorya-2 successfully tested gas with flow rates of 20 MMscf/d and 17 MMscf/d respectively, while Likonde-1 encountered gas shows. As a result, Ndovu applied to the Ministry of Energy for Tanzania in September 2017 for a 25-year development licence over the Ntorya area, with the application recommending the drilling of one well, the acquisition of 3D seismic over the Ntorya Field and the construction of a raw gas pipeline tied to the National Gas Gathering System at the Madimba plant, starting point of Mnazi Bay-Dar es Salam gas pipeline. In April 2020, Ndovu Resources secured a one-year extension of the Ruvuma Licence, almost three years after it applied for it. The extension did not provide enough time to complete the exploration programme, reason why new operator APT had to apply for another one which was secured a lot faster.

Read more »

President Buhari has signed Nigeria’s Petroleum Industry Bill into law

It took almost two decades, two historic crashes in commodity prices and two recessions for Nigeria to finally adopt its new Petroleum Industry Bill. Following its passing at both chambers of Parliament in July, the bill was officially signed into law by President Buhari today. The bill is expected to provide much-needed regulatory certainty for investors seeking to do business in Africa’s most populous nation. Nigeria has the world’s eight largest proven gas reserves and is Africa’s largest crude oil producer. However, years of under-investment have left production on a declining trend: in June of this year, Nigeria was producing only about 1.4m bopd and has not been producing over the 2m bopd threshold since 2012. A major factor to judge the efficiency and impact of the PIB will now be its ability to revive deep-water projects that have remained on the shelves for years. IOCs in Nigeria have discovered billions of barrels of oil equivalent offshore which have remained undeveloped because of market conditions and lack of a supportive regulatory framework. The passing of Nigeria’s Deep Offshore and Inland Basin Production Sharing Contract (Amendment) Act in late 2019 had only further jeopardized the economics of most of these discoveries by removing the water depth-based royalty and replacing it with a flat 10% royalty on all deep-water PSC. It had also introduced a price-based royalty adding 0 to 10% depending on the oil price. Will the PIB be able to revive the investment appetite of IOCs for those deep-water projects? Time will tell but time is also of the essence. Only the development of these discoveries has the power to significantly increase Nigeria’s output. Another crucial aspect to take into consideration is the security situation in the Niger Delta. Insecurity and vandalism there are one of the main reasons for investors shying away from Nigeria and for the exit of IOCs out of their onshore and shallow water licenses in the country. It remains until today a major factor preventing Nigeria’s hydrocarbons sector to realize its investment potential. Because host communities will not be receiving the share they asked for (2.5-3% instead of 10%), an appeasement in the Niger Delta is not certain. For the same reason, the PIB is not expected to slow down the pace of divestments by IOCs in the Niger Delta, although the same move will benefit indigenous players with cash at hand.

Read more »